Explainable Hybrid Graph Neural Networks for Financial Fraud Detection and Credit Risk Propagation

Keywords:

Financial Fraud Detection, Graph Neural Networks (GNN), Credit Risk Prediction, Explainable Artificial Intelligence (XAI), Risk Propagation, Temporal Graph Learning, Heterogeneous Graph ModelingAbstract

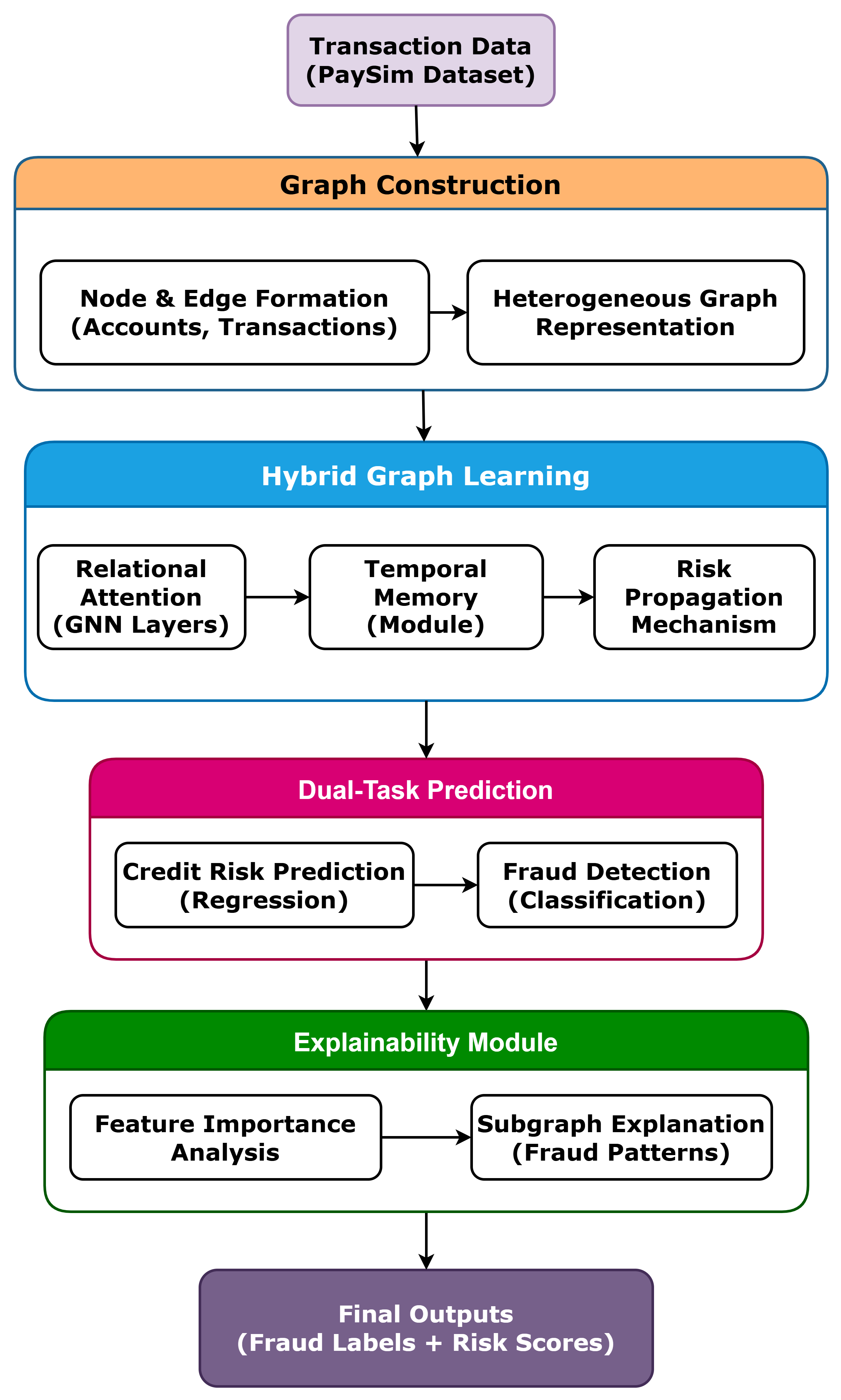

A rise of complex digital financial systems has prompted a surge of advanced fraudulent actions and escalating issues in proper credit risk evaluation. Conventional machine learning methods would tend to overlook the relational relationships and time dynamics of financial data, which leads to lower accuracy with detection limited and slower risk detection. To overcome these difficulties, we present in the current paper Explainable Hybrid Graph Neural Network (EH-GNN) model to do financial fraud early detection and credit risk propagation modeling. The proposed solution models financial transactions as a heterogeneous graph and incorporates a relational attention, time memory model, and risk propagation systems in the same architecture. It also includes a dual-task prediction module that simultaneously predicts fraud risk and credit risk as well as a multi-level explainability module that offers explainable understanding at a feature and a graph level. The proposed framework has been proved effective through extensive experiments carried out on the PaySim, and Credit Card Fraud Detection datasets. The EH-GNN has a higher accuracy of 98.6, F1-score of 0.93 and ROC-AUC of 0.968 compared to the state-of-the-art baseline models. Moreover, it minimizes the error in credit risk prediction with 0.089 RMSE which depicts a better reliability of Ms.Credit risk estimation. The findings support that the suggested framework is able to represent complicated financial dynamics and offer predictions that can be interpreted, hence is a powerful and viable way to apply to real-life fraud detection and risk management mechanisms.

Downloads

Published

Issue

Section

License

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License. You are free to share and adapt the material, but only for non-commercial purposes. You must give appropriate credit to the author(s).